Legal training by Hedman

https://drive.google.com/file/d/1nRQ5QOFRSsm_jgSyTuG-6G6yjOSuUqFm/view?usp=drive_link

Shareholders Agreement

Investment agreement

- warranties (company is established & not bankrupt)

- liability (data protection, EU grants)

Convertible note agreement / SAFE agreement

Convertible notes / loans

- investor gives a loan

- terms of conversion pre-agreed

- gets a promise - investor becomes a shareholder upon conversion of the loan, not immediately

- helps if the valuation is lower than desired

- Some variables:

- loan amount

- interest

- CAP (max valuation to convert to shares)

- discount (optional)

- maturity date (2-3 years)

- valuation floor

- most favoured nation

- information rights (what information is accessed)

- participation right

- future sha content

Reverse vesting

Share transactions

Preferential subscription rights

Term Sheet

- establish key conditions under which investment is made

- valuation

- investment amount

- special rights of the investor

- confidentiality, costs / obligations not to simultaneously hold investments talks with other investores

- usually driven by investor

Option pool

- non-monetary compensation

- attracting talent

- size varies depending on role

- the later you get options, the smaller the size is

- can be given to advisors

1st way to implement - Virtual option pool

- exists only in a spreadsheet

- not visible in the commercial registry

- easily manageable

- increase of share capital upon exercise

- does not create problems if not exercised to full extent

2nd way to implement - Treasury share as option pool

- acquiring the treasure share

- Notary appointment needed upon exercise in most cases

- calculation of votes is more complicated

3rd way - Option pool held by a shareholder

- creates problems

- voting rights (can’t split share votes)

- dividents

- partial exercising is problematic

- notary appointment needed

Taxation

- region-specific taxation rules

In Estonia:

- granting stock options = not taxed

- sale of stock options = taxed

- vesting of stock options = not taxed

- exercising of stock options

- exercising prior to 3 years

- Non-monetary renumeration / fringe benefit ~ 70% taxation

- income tax + social tax

- Non-monetary renumeration / fringe benefit ~ 70% taxation

- exercising after 3 years = not taxed

- exercising prior to 3 years

Taxation exceptions

- full company exit (2/3 of shares → 2/3 is not taxed)

- death or loss of capability to work

Non-compete

- Protecting the business and the advantages in the market

- different from the employment law non-compete

Non-solicitation

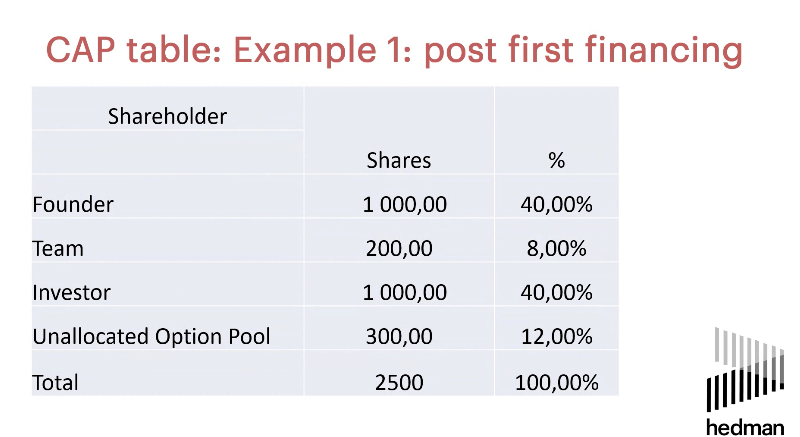

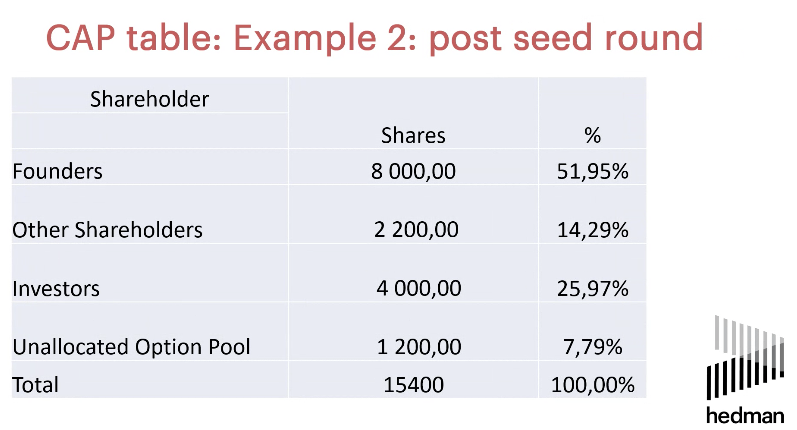

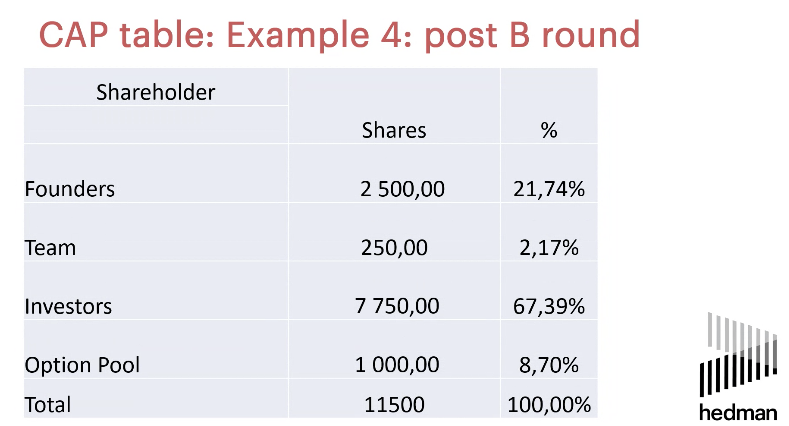

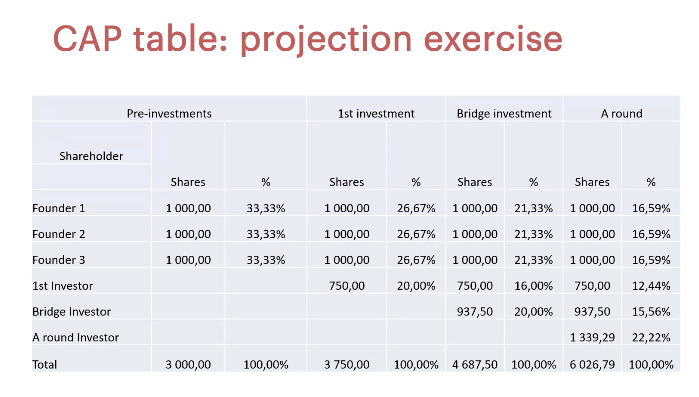

CAP table

- shows equity capitalization of the company

- Usually Excel or custom software

- Projections on future rounds